- News

- Basics

- Products

- JP Job shop

- Exhibition

- Interview

- Statistic

- PR

- Download

- Special contents

![]()

Japanese Cutting-Edge

Japanese Cutting-Edge

Solutions for Metalworking

![]() Japanese Cutting-Edge

Japanese Cutting-Edge

Solutions for Metalworking

Statistic

August 9, 2023

Japan’s machine tool orders are gradually declining in 2023, compared with last year’s strong performance in 2022. Still, the order level itself is still high, as it continues to meet the “100 billion yen or more per month” standard, which is considered a benchmark for favorable or unfavorable conditions. Comparing domestic and foreign demand, the decline in domestic demand is more pronounced due to the high dependence on the automobile industry. However, domestic automobile production is recovering and there are signs of a comeback in the second half of this year. There are also expectations of more and serious investment in electric vehicles (EVs).

According to the Japan Machine Tool Builders’ Association (JMTBA), the total amount of orders received for machine tools in May this year was 119.5 billion yen. This is a decrease of 9.9% from the previous month, a decrease of 22.1% from the same month last year, and the first time in 27 months that orders have fallen below 120 billion yen. However, the level of “orders exceeding 100 billion yen in a single month,” which is considered a rough indicator of favorable or unfavorable conditions, has remained high for 28 consecutive months.

For June, the total amount of orders received in the first half of this year fell 15.7% year-on-year (YoY) to 768.44 billion yen, showing a clear sign of slowdown. Domestic demand fell 19.9% YoY, while foreign demand fell 13.5% YoY, with the decline in domestic demand more pronounced than that in foreign demand.

Domestic demand for May totaled 37.8 billion yen, down 9.4% from the previous month and down 23.6% from the same month last year, falling below 40 billion yen for the first time in three months, the second consecutive month-on-month (MoM) decline, and the ninth consecutive MoM decline. Factors contributing to the MoM decline included a decrease in operating days due to a major national holiday and the loss of subsidy effect.

Looking at trends by industry since January this year, overall conditions have been declining since the second half of last year. Although they picked up in March due to the effect of the fiscal year-end, they have been slowly declining since then. This trend is particularly evident in the major sectors of general industrial machinery, automobiles, and electrical/precision machinery.

Japan is said to be lagging behind the rest of the world in terms of recovery from the COVID-19 pandemic and in terms of full-scale investment in EVs. Last fall, the 31st Japan International Machine Tool Fair (JIMTOF 2022) was held for the first time in four years, and MECHATRONICS TECHNOLOGY JAPAN 2023 (MECT2023) is scheduled for this fall. It is hoped that the presence of a major exhibition useful for the machine tool business will be a catalyst for demand.

The industries that have the biggest impact on the Japanese market today are automobiles and semiconductors, and many believe that trends in EVs and semiconductor manufacturing equipment in particular could be key to the ups and downs of the second half of this year. This is because both industries are expected to grow and recover as early as this time.

The industries that have the biggest impact on the Japanese market today are automobiles and semiconductors, and many believe that trends in EVs and semiconductor manufacturing equipment in particular could be key to the ups and downs of the second half of this year. This is because both industries are expected to grow and recover as early as this time.

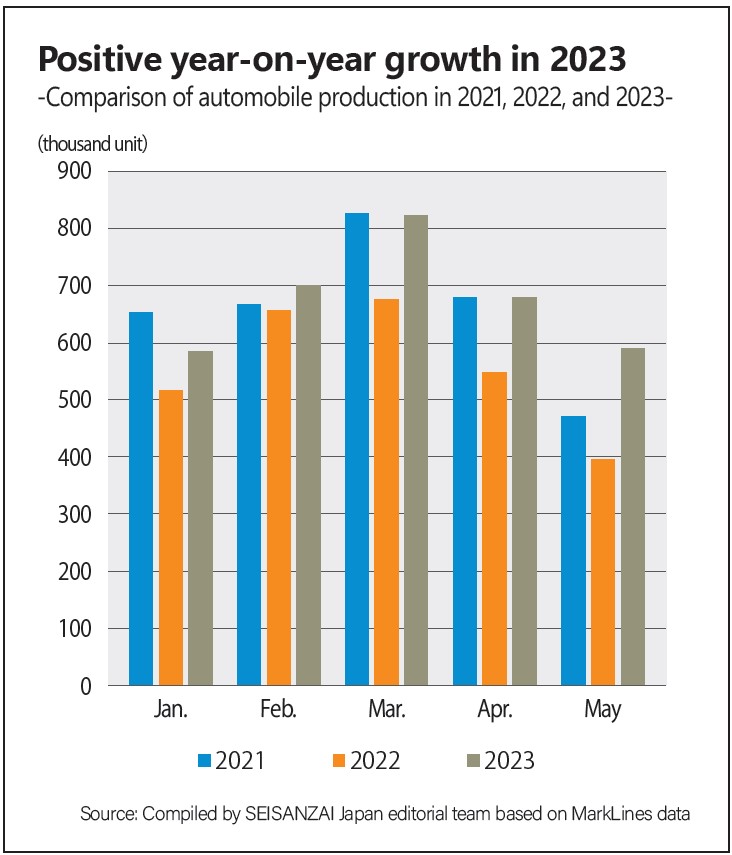

According to data from passenger car manufacturers, domestic production was 585,000 units in January, 701,000 units in February, 824,000 units in March, 680,000 units in April and 590,000 units in May this year, all of which are positive growth compared to the same period last year. Last year, the semiconductor supply shortage took a heavy toll on the production volume. This year, however, the situation has improved and stabilized, and there are signs that production is increasing without significant cutbacks.

Japan is heavily dependent on the automobile industry, and if automobile production increases, the manufacturing industry should be in good shape. Expectations are rising not only for EVs, but for the industry in general, with some saying, “We are starting to see such an upward trend in the second half of this year.”

Investment in EVs is also eagerly anticipated. Many in the industry argue that investment in EVs begins and really takes off this year, peaking in a few years. There is, of course, the possibility that various factors will delay plans and push the start of full-scale investment into next year. Nevertheless, expectations are high that the start of investment in EVs is imminent, and it seems likely that preparations can move forward.

Investment expectations are not limited to EVs. Investment in the development of new technologies (e.g. green), supply chain strengthening, automation and efficiency improvements is also likely to remain strong. These issues are not limited to the automotive industry, but are important to all industries, so movement is expected, whether for new projects or renewals.

A large number of visitors attended JIMTOF 2022 last year.

How about semiconductors? There is some good news: Taiwan Semiconductor Manufacturing Company (TSMC), the world’s largest semiconductor foundry, is currently building its first plant in Kumamoto Prefecture, southern Japan, and plans to begin construction of a second plant, also in Kumamoto Prefecture, in April 2024.

In July, the Semiconductor Equipment Association of Japan (SEAJ) released its demand forecast for semiconductor production equipment, forecasting that sales of Japan-made equipment will decline 23% YoY to 3,201.1 billion yen in FY2023 as capital investment, particularly in memory, is slow to recover.

In the following fiscal year, FY 2024, memory is expected to recover and logic-related capital spending is also expected to recover. As new central processing units (CPUs) are introduced, the use of generative artificial intelligence (AI) such as “Chat GPT” expands, and investment in servers for data centers continues, demand is expected to increase 30% year on year to ¥3,926.1 billion. Strong investment trends are forecast to continue through FY2025.

Demand for machine tools is also expected to increase in line with the growth in demand for semiconductor production equipment. Equipment manufacturers are currently in the midst of an inventory adjustment phase, but as business recovers, the contract manufacturing industry should recover, which in turn should spur investment mainly in automation and efficiency improvements. Mr. Akihide Kobayashi, Secretary General of SEAJ, said, “The recovery (of the manufacturing equipment industry) is likely to take place in the fall or winter of this year. Because generative AI requires large amounts of semiconductors, investment in these applications is also active, and demand may peak before other areas.“

The second half of this year should be closely watched with high expectations for both automobiles and semiconductors.

Share On :