- News

- Basics

- Products

- JP Job shop

- Exhibition

- Interview

- Statistic

- PR

- Download

- Special contents

![]()

Japanese Cutting-Edge

Japanese Cutting-Edge

Solutions for Metalworking

![]() Japanese Cutting-Edge

Japanese Cutting-Edge

Solutions for Metalworking

Statistic

December 5, 2024

By: Atsushi Mizuno, Staff Editor, SEISANZAI Japan

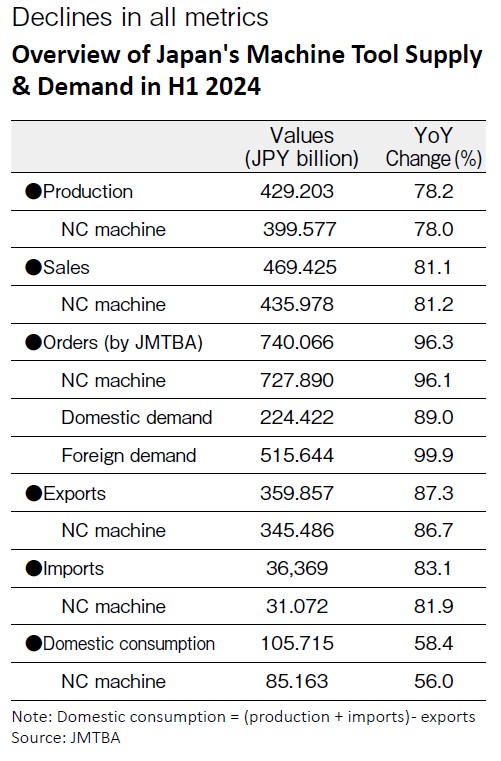

The supply and demand performance of machine tools and forging machines in the first half of 2024 (January-June) has been summarized. According to the Japan Machine Tool Builders’ Association (JMTBA), Japan’s machine tool orders decreased by 3.7% year-on-year (YoY) to 740.066 billion yen, while production value decreased by 21.8% YoY to 429.203 billion yen. Despite the global economic slowdown, both orders and production showed resilience and avoided sharp declines.

The global economy faced a slowdown in the first half of 2024, but avoided a major downturn. In the United States, significant interest rate hikes to curb inflation have led to growing fears of a recession. Meanwhile, China’s economic slowdown, linked to the downturn in its real estate market, has continued. Despite these headwinds, the global economy remained on a stable growth path.

The global economy faced a slowdown in the first half of 2024, but avoided a major downturn. In the United States, significant interest rate hikes to curb inflation have led to growing fears of a recession. Meanwhile, China’s economic slowdown, linked to the downturn in its real estate market, has continued. Despite these headwinds, the global economy remained on a stable growth path.

Japan’s economy followed a similar trend, with major corporations steadily advancing their capital investment plans despite global market pressures.

According to the “Corporate Enterprise Sentiment Survey” released by Japan’s Cabinet Office and Ministry of Finance on September 12, capital investment for fiscal 2024 is projected to increase 12.5% YoY. In the manufacturing industry, the increase is expected to be 15.9% YoY, with the “automobile and automobile parts manufacturing” sector-a major user of machine tools and forging machines-anticipating an increase of 21.1% YoY.

While the outlook for capital investment is bright, the machine tool market has struggled in the first half of the year. Data from the JMTBA’s Machine Tool Supply and Demand Trends and Metalworking Machinery Statistics show that all metrics – production, sales, orders, exports, imports, and domestic consumption – were below the levels of the previous year.

Total new orders for machine tools in the first half of 2024 fell 3.7% YoY to 740.066 billion yen, marking the second consecutive year of decline.

Total new orders for machine tools in the first half of 2024 fell 3.7% YoY to 740.066 billion yen, marking the second consecutive year of decline.

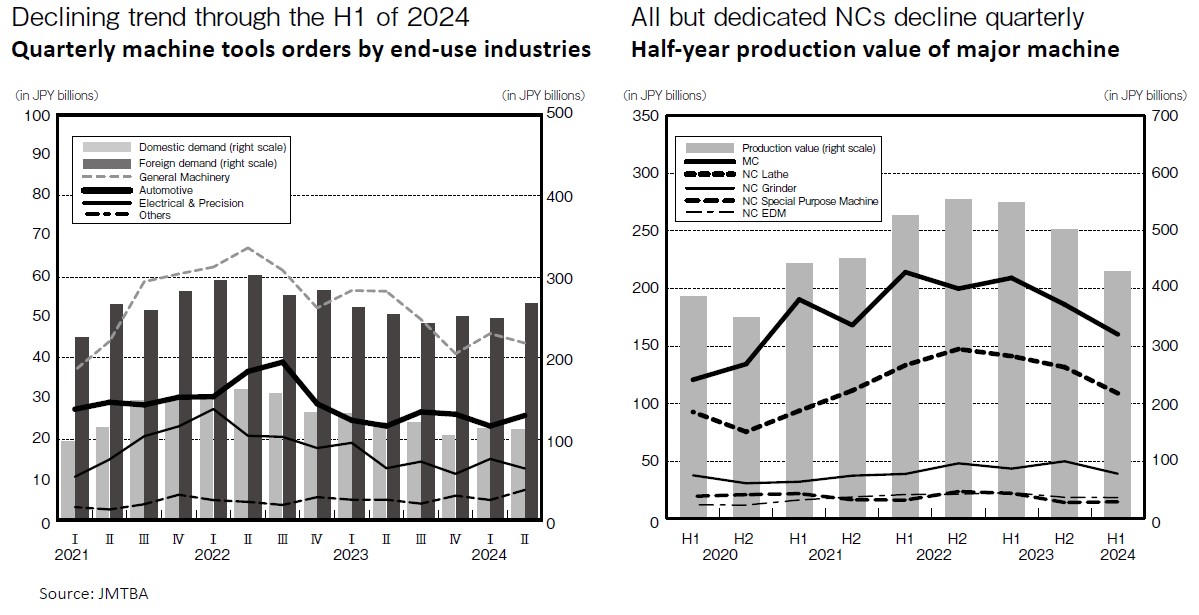

Although orders have been declining since the record-high levels of 2022, they have remained robust. Monthly orders exceeded the 100 billion yen benchmarks, considered a sign of strong demand, in every month of the first half. In May and June, orders even exceeded the previous year’s levels, driven by overseas demand.

Domestic orders fell 11.0% YoY to 224.422 billion yen. Among the 11 major demand industries, roughly half posted YoY growth. While orders from the “General Machinery” sector fell 20.7%, the “Automobiles” sector posted a modest increase of 2.5%, and the “Aircraft, Shipbuilding & Transportation Machinery” sector surged 23.3%, reflecting significant differences in performance across industries.

Foreign orders remained almost flat, declining 0.1% YoY to 515.644 billion yen. While orders from Asia increased slightly, declines in North America and Europe weighed on overall performance.

Asia: Up 6.3% YoY to 243.361 billion yen. Orders from China, the largest market, were up 3.4% YoY, with increases also recorded in South Korea and Taiwan. Thailand and Vietnam were also favorable, while India stood out with a 20.1% YoY increase.

North America: Decreased 1.8% YoY to 152.124 billion yen. Although orders from Canada and Mexico increased, orders from the United States decreased 5.1% YoY to 131.720 billion yen.

Europe: Down 13.1% YoY to 102.653 billion yen. While countries such as France showed slight growth, many markets, particularly Germany and Italy, recorded declines.

The production value of Japan’s machine tools in the first half of 2024 fell 21.8% YoY to 429.203 billion yen, with production volume down 27.1% YoY to 23,706 units. Most categories, including lathes and machining centers (MCs), showed declines. However, the average price per machine increased 7% YoY to 18.1 million yen.

Among specific categories:

NC vertical lathes, NC drilling machines and NC boring machines saw YoY increases in production value.

The recent trend of increasing production of large MCs, such as gantry-type machines, was reversed, however, as production of MCs with strokes less than 500 mm and table sizes less than 500 mm both fell sharply by 30.4% YoY.

Grinding machines fell 10.6% YoY to 46.337 billion yen, with NC cylindrical grinders down 1.7% and NC surface grinders down 19.1%.

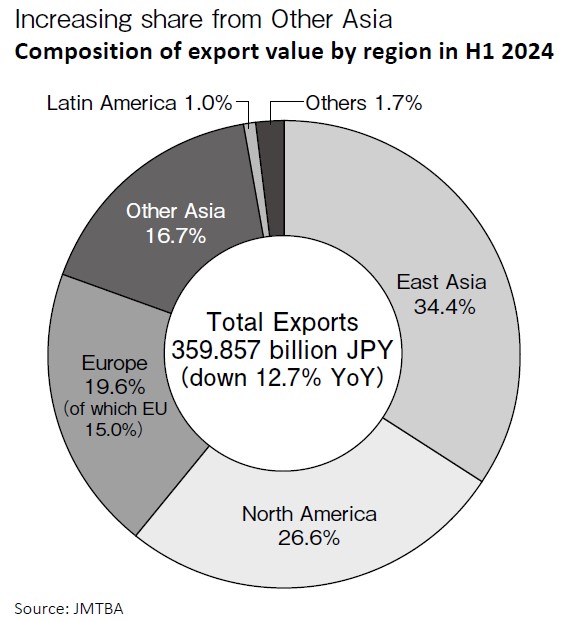

Machine tool exports decreased 12.7% YoY to 359.857 billion yen, with the export volume decreasing 7.5% YoY to 30,839 units.

Machine tool exports decreased 12.7% YoY to 359.857 billion yen, with the export volume decreasing 7.5% YoY to 30,839 units.

Regionally, East Asia accounted for the largest share at 34.4%, but this was down 0.6 percentage points from the previous year. North America followed with 26.6% (down 1.6 points) and Europe with 19.6% (down 1.6 points). Other Asia rose to 16.7%, an increase of 3.5 points.

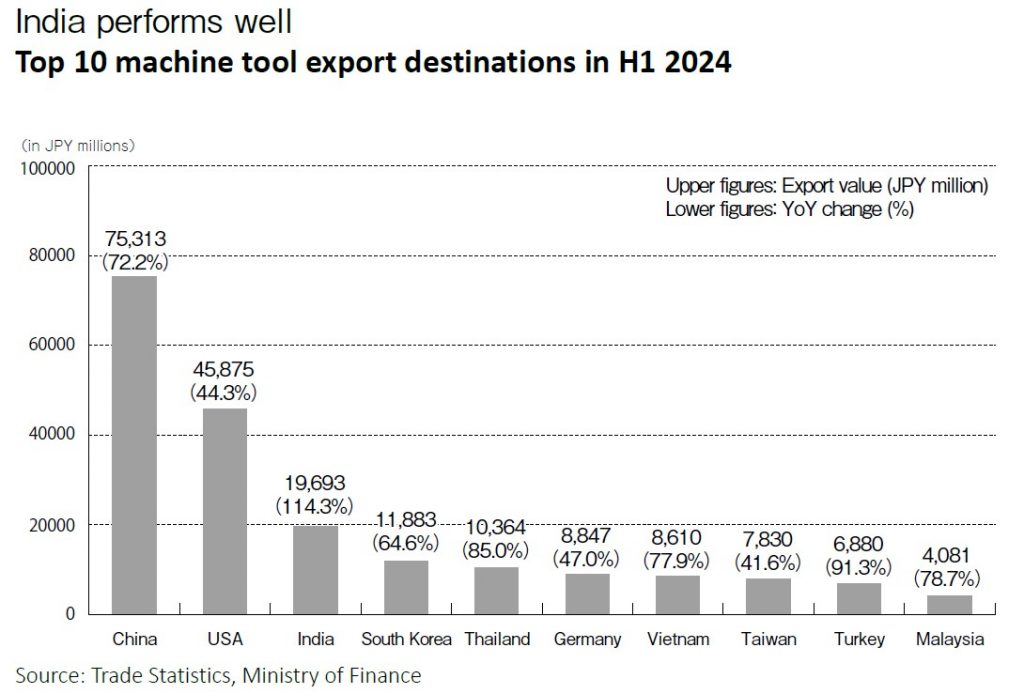

Top 10 export markets: China remained the largest market despite a 27.8% YoY decline to 75.313 billion yen, followed by the U.S., which experienced a steep 55.7% YoY decline to 45.875 billion yen. India climbed to third place with a 14.3% YoY increase, followed by South Korea and Thailand. Germany, which ranked third last year, fell to sixth place with a 53% YoY decline.

By machine type, five-axis or more vertical MCs increased by 8.0% YoY and five-axis or more horizontal MCs increased by 33.5% YoY, while major categories such as lathes and laser processing machines declined. Laser processing machines, in particular, dropped 29.1% YoY.

By machine type, five-axis or more vertical MCs increased by 8.0% YoY and five-axis or more horizontal MCs increased by 33.5% YoY, while major categories such as lathes and laser processing machines declined. Laser processing machines, in particular, dropped 29.1% YoY.

In addition, SEISANZAI Japan has independently compiled the top 10 export destinations for major machine types, particularly NC lathes and machining centers (MCs), based on the Ministry of Finance’s “Trade Statistics”.

For NC lathes, the United States ranked first, followed by China, as in the previous year. However, Germany, which ranked fifth in the previous year, moved up to third place. Mexico also showed significant growth over the previous year, moving up to eighth place.

For NC lathes, the United States ranked first, followed by China, as in the previous year. However, Germany, which ranked fifth in the previous year, moved up to third place. Mexico also showed significant growth over the previous year, moving up to eighth place.

For MCs, the top three countries remained unchanged from last year: China, the United States, and India. Export values declined for China (down 11.5% YoY to 52.1 billion yen) and the United States (down 17.3% YoY to 34.9 billion yen), while India recorded a 20.3% YoY growth to 11.4 billion yen.

Despite the overall downward trend in exports, India’s strong performance underscored its presence as a growing market.

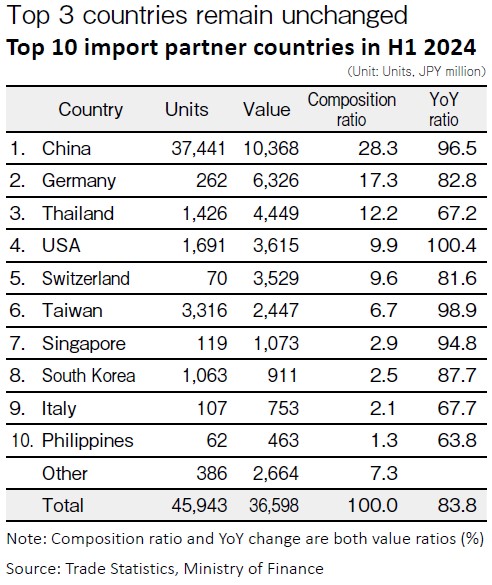

Machine tool imports fell 16.9% YoY to 36.369 billion yen, with the volume decreasing 4.3% YoY to 47,333 units. Japan’s imports are skewed toward non-NC machines, which accounted for 77.5% of the import volume and only 14.5% of the total import value in the first half of 2024.

Machine tool imports fell 16.9% YoY to 36.369 billion yen, with the volume decreasing 4.3% YoY to 47,333 units. Japan’s imports are skewed toward non-NC machines, which accounted for 77.5% of the import volume and only 14.5% of the total import value in the first half of 2024.

China, Germany and Thailand remained the top import sources. The United States showed a stable performance with a slight increase of 0.4%.

Among different types of machines, NC surface grinders and NC cylindrical grinders exceeded the previous year’s levels. In contrast, lathes decreased by 13.7% YoY and special machine tools, including NC laser machine tools, decreased by 27.6% YoY.

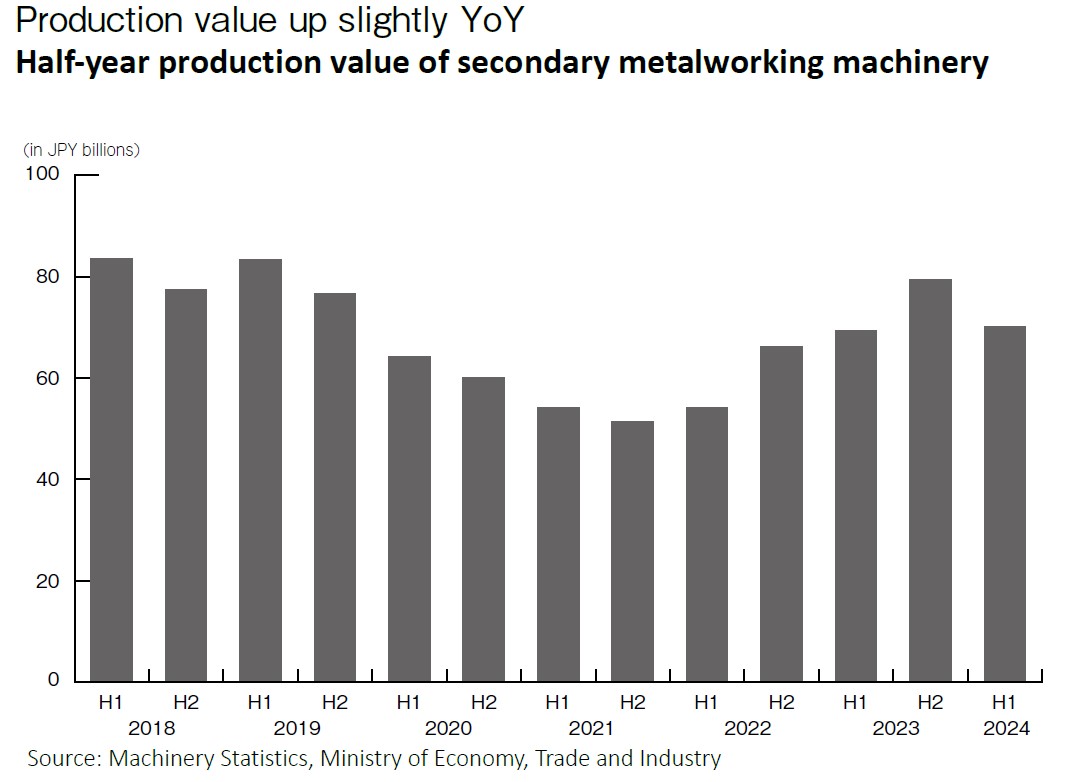

According to the Ministry of Economy, Trade and Industry’s “Machinery Statistics,” the production value of secondary metalworking machines – such as press brakes and bending machines – was 70.13 billion yen in the first half of 2024, a slight increase of 0.8% YoY. However, the production volume decreased by 18.7% YoY to 2,258 units.

According to the Ministry of Economy, Trade and Industry’s “Machinery Statistics,” the production value of secondary metalworking machines – such as press brakes and bending machines – was 70.13 billion yen in the first half of 2024, a slight increase of 0.8% YoY. However, the production volume decreased by 18.7% YoY to 2,258 units.

By machine type, bending machines increased by 11.5% YoY, while hydraulic presses increased by 22.2% YoY. Conversely, mechanical presses decreased by 3.6% to 45.89 billion yen.

According to the Japan Forming Machinery Association, total orders for forming machinery (including press machines, sheet metal machines and services) amounted to 174.16 billion yen in the first half of 2024, down 6.2% YoY. On a monthly basis, only April exceeded the previous year’s level, while other months fell short. Press-related orders decreased 12.4% YoY to 67.67 billion yen, and sheet metal-related orders decreased 10.5% YoY to 57.83 billion yen.

The global economic slowdown affected orders in the first half of 2024, but performance remained stable. From July to October, orders showed a mixed trend:

July: Up 8.4% YoY to 123.942 billion yen.

August: Down 3.5% YoY to 110.770 billion yen.

September: Down 6.4% YoY to 125.360 billion yen.

October: Up 9.4% YoY to 122.550 billion yen.

Looking ahead, economic recovery is expected later this year and into 2025. In the United States, the Federal Reserve’s September interest rate cut, the first in four years, is expected to boost capital investment. In China, subsidies for equipment upgrades have begun to show results, and machine tool orders are on the rise.

The Japan International Machine Tool Fair (JIMTOF) in November saw active business discussions, raising expectations of a recovery in the Japanese market.

However, global economic risks, including geopolitical tensions, interest rate policies, and the impact of the U.S. presidential election, require careful monitoring.

February 16, 2024

September 24, 2025

Share On :