- News

- Basics

- Products

- JP Job shop

- Exhibition

- Interview

- Statistic

- PR

- Download

- Special contents

![]()

Japanese Cutting-Edge

Japanese Cutting-Edge

Solutions for Metalworking

![]() Japanese Cutting-Edge

Japanese Cutting-Edge

Solutions for Metalworking

Statistic

August 25, 2023

Southeast Asia is home to many Japanese companies due to its geographical proximity to Japan and abundant labor force. The demand for machine tools in the region is also high, making it one of the most important markets for the Japanese machine tool industry. Although the current order trend is above the pre-COVID-19 pandemic level, there are signs of a gradual slowdown, with orders falling below the previous year’s level for four consecutive months. However, Southeast Asia is attracting attention from companies around the world as “the world’s factory” next to China, and demand for semiconductor production equipment and electric vehicles (EVs) is expected to increase in the future.

The pace of economic growth in Southeast Asia is decelerating in the wake of the global economic slowdown.

According to the Japan External Trade Organization (JETRO), Thailand was the only country among the six major Southeast Asian countries (Thailand, Malaysia, Indonesia, Vietnam, the Philippines and Singapore) whose actual gross domestic product (GDP) growth rate in the first quarter of 2023 was higher than that of the previous quarter, while the remaining five countries experienced slower growth than that of the previous quarter.

As in other major markets such as Europe, the U.S., and Japan, inflationary trends and currency depreciations have continued in Southeast Asia, and central banks in each country have implemented a series of tight monetary policies to control price increases from last year to this year. As a result, demand for consumer spending and corporate capital investment also weakened.

Demand for machine tools in Southeast Asia also began to slow this year. According to the Japan Machine Tool Builders’ Association (JMTBA), the total amount of monthly orders received from the six major Southeast Asian countries fell below the previous year’s level for four consecutive months from February to May 2023.

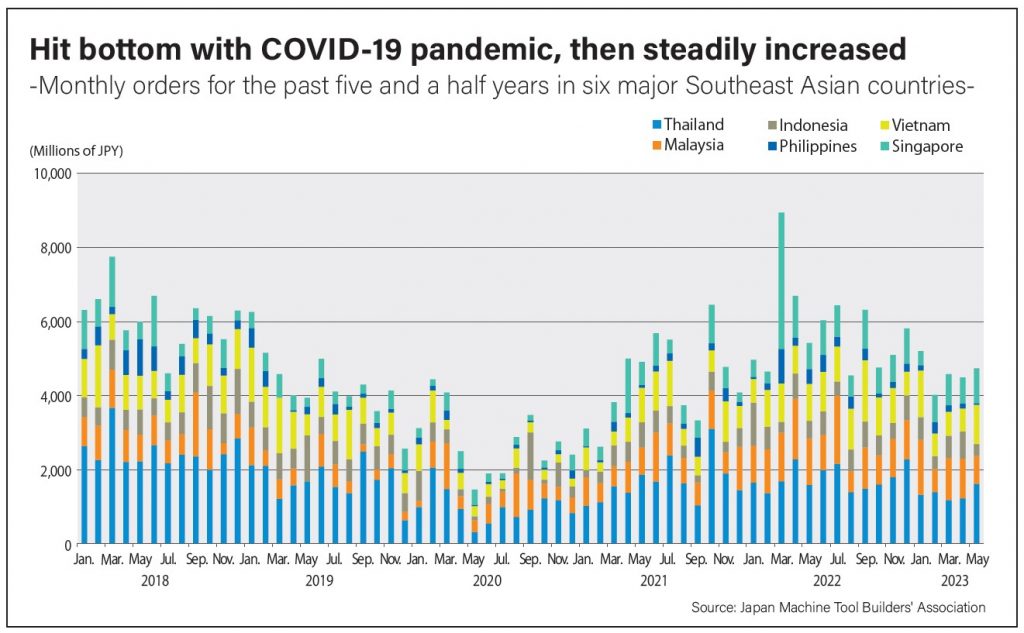

The chart below shows the monthly order amount for the past five and a half years for six major Southeast Asian countries, according to the JMTBA. In 2018, when the machine tool industry as a whole was booming, demand was strong, particularly in Thailand, with some months notable for exceeding 6 billion in total for the six major countries. However, in 2019, trade tensions between the US and China intensified, and the economies of Southeast Asia, which were highly dependent on the Chinese economy, slowed down. Machine tool orders also declined steadily.

In 2020, the COVID-19 pandemic followed suit, bottoming out at 1.46 billion yen in May. Since then, machine tool orders have risen steadily in line with the resumption of economic activity, reaching a peak of 8.951 billion yen in March 2022, the highest in the past five and a half years.

Beginning in 2023, orders received from the six major countries from Japan remained higher than those received in 2019 before the COVID-19 pandemic. However, as noted above, the momentum in orders has gradually begun to show signs of slowing, with four consecutive months of year-on-year declines.

Among the six major countries in Southeast Asia, Thailand is the market with the largest demand for machine tools. The Thai machine tool market is characterized by a strong dependence on Japan for both machine imports and exports, and a large number of Japanese machine tool builders and machine trading companies have established production bases and local subsidiaries in the country to capture local needs.

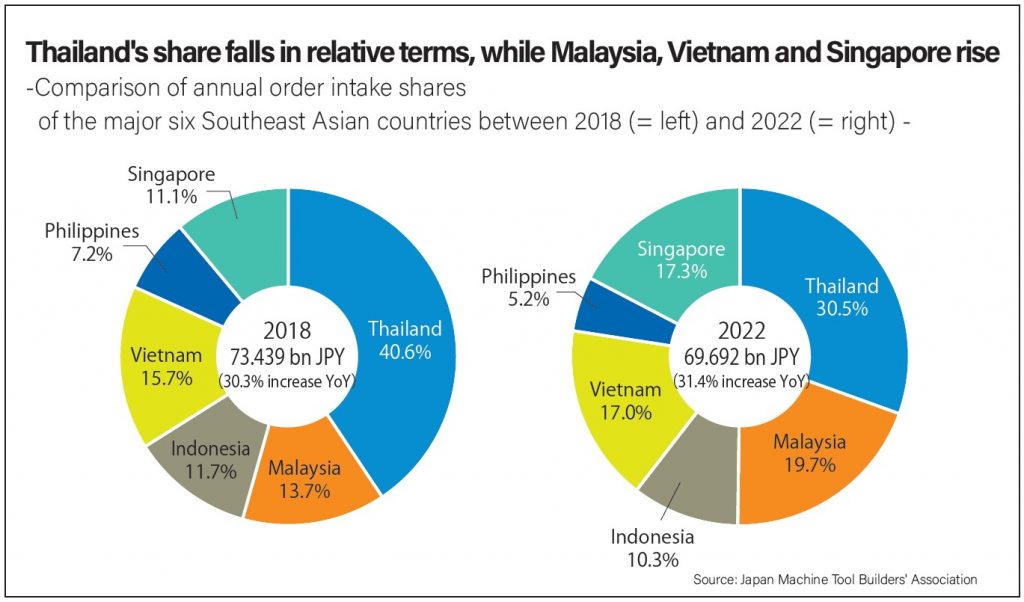

The two pie charts below show the percentage of orders received from the six major countries in 2018 (=left) and 2022 (=right), when the machine tool industry was strong. In both cases, Thailand retained the top share, but last year it was 30.5% compared to 40.6% in 2018, a drop of 10.1 percentage points from 2018.

While Thailand has lost relative share, Malaysia, Vietnam and Singapore have emerged as newcomers to the market. In particular, machine tool orders from Malaysia increased significantly last year; the country’s share of total orders from the top six countries was 13.7% in 2018, but increased by 6.0 percentage points to 19.7% last year.

Southeast Asia is currently attracting a lot of attention from automotive and semiconductor manufacturers around the world as the “world’s factory” next to China. Against the backdrop of escalating trade tensions between the US and China, many manufacturers have shifted their production bases from China to Southeast Asia in recent years. Malaysia and Vietnam have thriving electronics industries, including semiconductors, and the increase in the share of machine tool orders from both countries is believed to be driven by semiconductor-related demand. Given this trend of supply chain reorganization, the markets in both countries are likely to continue to see strong demand for machining parts for semiconductor production equipment.

In addition, Thailand and Indonesia, which drive the economies of Southeast Asia, have active automotive industries. Thailand, in particular, is known as the “Detroit of Asia,” and automotive-related manufacturers from around the world, particularly Japanese companies, are moving into the country.

The automotive industry is facing a “once-in-a-century transformation period,” and a shift to EVs is also underway in both countries. For example, BYD, a major Chinese EV manufacturer, has established a finished vehicle plant in Thailand as its first overseas production base, and there has been a particularly noticeable move by Chinese manufacturers to set up production bases in the region. As an EV-focused supply chain is established in Southeast Asia, machine tool demand is expected to gradually shift from conventional internal combustion engine vehicles to EVs. Demand for EV-related parts machining is already growing in Thailand, and Indonesia is known as the world’s largest producer of nickel, which is used in lithium batteries for EVs. Both markets are therefore expected to see significant EV-related investment in the future.

Share On :