- News

- Basics

- Products

- JP Job shop

- Exhibition

- Interview

- Statistic

- PR

- Download

- Special contents

![]()

Japanese Cutting-Edge

Japanese Cutting-Edge

Solutions for Metalworking

![]() Japanese Cutting-Edge

Japanese Cutting-Edge

Solutions for Metalworking

Statistic

May 25, 2026

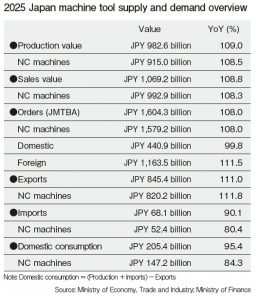

Japan’s machine tool industry returned to growth in 2025, with total orders reaching JPY 1,604.3 billion — the fourth-highest level on record. Production also grew for the first time in three years, rising 9.0% to JPY 982.6 billion. Foreign demand drove the recovery, while domestic demand remained sluggish.

This report covers Japan’s machine tool supply and demand figures for 2025, drawing on two sources:

– Production data: Ministry of Economy, Trade and Industry (METI) Production Dynamic Statistics

– Order data: Japan Machine Tool Builders’ Association (JMTBA)

Together, these figures provide a comprehensive picture of production, domestic and foreign orders, exports, and imports across machine tool categories.

Japan is one of the world’s leading machine tool producers, and its order data is widely watched as an indicator of global manufacturing investment trends. The 2025 results are significant for several reasons:

– Foreign orders reached a new all-time high, exceeding JPY 1,160 billion for the first time

– Five-axis and above MC orders grew 28.1%, reflecting demand for higher-capability equipment

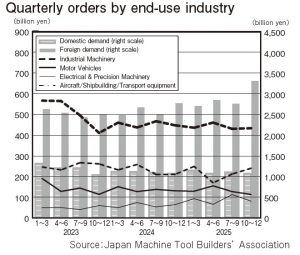

– Aircraft/Shipbuilding/Transport Equipment set a domestic record, up 45.8%

– The latest March 2026 orders surpassed the previous monthly record set in March 2018

At the same time, domestic demand fell below JPY 450 billion for the second consecutive year, and the order backlog declined for the third straight year — signals that the recovery remains uneven.

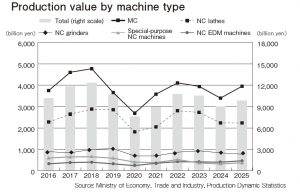

Machine tool output rose 9.0% YoY to JPY 982.6 billion, with NC machine output up 8.5% to JPY 915.0 billion.

Machining centers were the standout category, rising 15.4% to JPY 392.1 billion. Vertical MCs accounted for approximately 60% of that total, up 21.8% to JPY 234.8 billion. Horizontal MCs were broadly flat at JPY 106.1 billion, while other MCs including gantry types surged 31.3% to JPY 51.2 billion.

Lathes declined 3.5% to JPY 233.7 billion, and NC grinding machines fell 7.3%. Smaller categories showed divergence: NC electrical discharge machines rose 15.6% and NC special-purpose machines gained 14.5%.

NC machine domestic consumption, calculated as production plus imports minus exports, fell 15.7% to JPY 147.2 billion.

Total orders of JPY 1,604.3 billion exceeded the prior-year level in every month except June, with March and December each surpassing JPY 150 billion.

Domestic orders edged down 0.2% to JPY 440.9 billion. Industrial Machinery fell 2.9%, Motor Vehicles declined 4.3%, and Electrical & Precision Machinery dropped 4.0%. Aircraft/Shipbuilding/Transport Equipment was the exception, surging 45.8% to a record high.

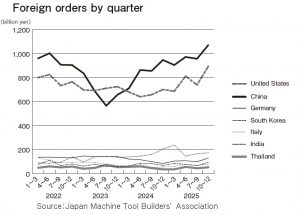

Foreign orders rose 11.5% to a record JPY 1,163.5 billion.

– Asia: up 12.2% to JPY 580.2 billion. China recovered strongly, up 15.7% to a record JPY 390.1 billion, driven by automotive and electronics demand. Korea, India, and Singapore also posted gains.

– North America: up 17.6% to a record JPY 360.0 billion, with the U.S. up 17.0% to JPY 312.7 billion. Aerospace, construction machinery, and automotive all contributed. Mexico extended its growth streak to five consecutive years.

– Europe: up 4.5% to JPY 197.4 billion, returning to growth but remaining below JPY 200 billion. Germany recovered only modestly, up 4.7%.

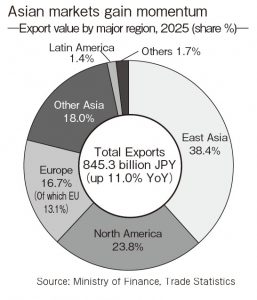

Machine tool exports rose 11.0% to JPY 845.4 billion, with NC machine exports up 11.8% to JPY 820.2 billion — the first increase in three years.

By region, Asia led with a 21.5% increase to JPY 476.6 billion. East Asia’s share of total exports reached 38.4%, maintaining its top position for the fifth consecutive year. Other parts of Asia also increased, while North America and Europe both declined from the previous year.

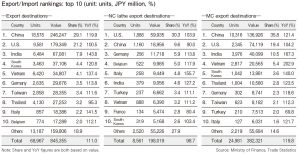

By country, China topped the rankings for the second consecutive year, up 19.9% to JPY 246.2 billion. Vietnam was the standout mover, climbing to fifth place with growth of 102.9%.

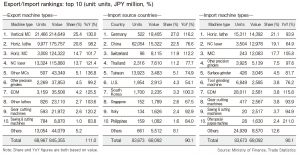

By machine type, vertical MCs surged 30.0% to claim the top export position for the first time in four years.

Machine tool imports fell 9.9% to JPY 68.1 billion. Germany overtook China as the top import source, rising 16.2% to JPY 18.4 billion. China fell to second place, down 23.4%. The top four sources combined accounted for 72.6% of total imports.

The 2025 figures show that the recovery is being led by foreign demand, while domestic demand remains weak. The record March 2026 orders suggest momentum is continuing into 2026, but the operating environment is becoming more complex: tensions around the Strait of Hormuz threaten energy costs, and supply conditions for tungsten and other materials have tightened. The industry’s ability to read these shifts and respond quickly will matter as much as the demand numbers themselves.

February 18, 2026

Share On :